Income Types and How They're Taxed

The basic income categories that shape your federal tax bill

It’s tax season, a good time to step back and talk about how taxes work. We’ll start with federal taxes and build shared vocabulary before looking at how taxes can differ between households.

Taxes Are (Usually) Your Biggest Expense

For most households, taxes are the single largest expense each year.

Reducing your tax bill starts with understanding the system — and the first rule is simple: not all income is taxed the same.

Let’s briefly walk through the most common income types most households encounter, and how the IRS treats each one.

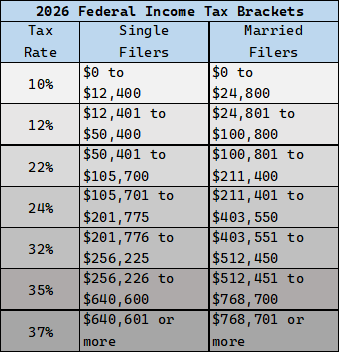

Wages

Income earned from an employer in exchange for your time and labor.

This is the most familiar — and often the most heavily taxed — form of income.

In addition to federal income tax, wages are subject to payroll taxes: Social Security and Medicare.

In 2026, Social Security tax is withheld at 6.2% on wages up to $184,500. Wages above that amount are not subject to Social Security tax.

In 2026, Medicare tax is withheld at 1.45% on all wages, with no income cap. An additional 0.9% Medicare surtax applies to wages above $200,000 for single filers and $250,000 for married couples filing jointly.

Interest

Income earned from lending money, such as through savings accounts, CDs, and bonds.

Interest is generally taxed like wages.

Short-Term Capital Gains

Profits from selling an investment held for 365 days or less.

The IRS taxes these the same way it taxes wages and interest.

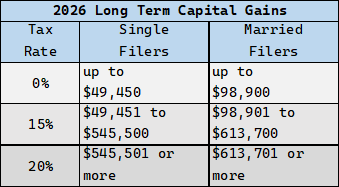

Long-Term Capital Gains

Profit from selling an asset held for more than 365 days, such as stock in publicly-traded companies.

These gains receive more favorable tax treatment than wages or short-term gains.

An additional 3.8% Net Investment Income Tax (NIIT) applies to investment income for single filers with income above $200,000 and married couples filing jointly with income above $250,000.

Qualified Dividends

Some companies pay dividends to their shareholders, which are cash payments made per share, often quarterly. Dividends that meet specific IRS requirements — including a minimum holding period — qualify for the same tax treatment as long-term capital gains.

Collectibles

Assets like art, gold, silver, and certain coins fall into a special tax category. Even when held long term, they’re taxed differently — and often less favorably — than stocks. Long-term gains on collectibles are taxed at rates up to 28% and may also be subject to the Net Investment Income Tax (NIIT).

Cryptocurrency

Crypto is treated as property, not currency.

Buying, selling, or trading can trigger capital gains or losses.

Income We’re Skipping (For Now)

Real estate ownership and operating a business both come with significant tax advantages — and major complexity.

They deserve their own posts, so we’ll leave them out for now.

Key Takeaway

The U.S. tax code taxes labor income more heavily and long-term investment income more favorably in order to encourage investment.