The Financial Advantage You Lose With Age

The underappreciated power of starting early

When you start earning money, it feels like freedom. You finally get to decide what to do with it - and naturally, your mind goes to the things you can buy today.

But here’s what isn’t discussed nearly enough: the youngest years of earning are the most valuable financial years. A simple habit of investing, when started early, can outweigh decades of greater effort later on.

Many people reach midlife wishing they had started earlier. By investing from a young age - even in small amounts - you can dramatically improve the odds of having enough in your sixties, or even earlier. When investing is done consistently over long periods of time, the benefit of time really adds up.

This is the power of compound interest. It’s often called the eighth wonder of the world, and a few charts will illustrate why.

We’ll cover specific investment options in future posts. For now, let’s keep things simple and assume an investment that earns a 9% annual return.

If you’re not familiar with the term return, think of a savings account that pays 9% interest per year. Deposit $1,000 on January 1st, and by the next New Year, that $1,000 has grown to $1,090.

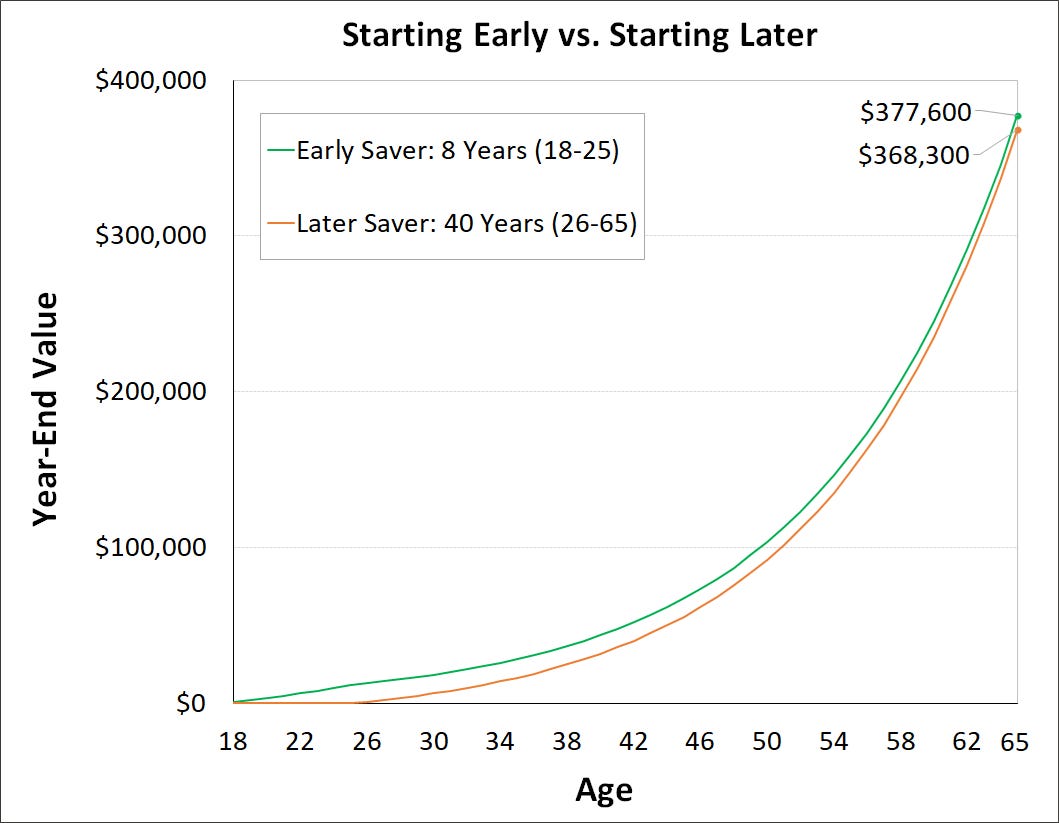

The chart below compares two investors. The first invests $1,000/year for eight years starting at age 18, then stops and lets the money grow until age 66. The second waits until age 26 and invests $1,000/year every year until age 66.

Despite contributing just $8,000 in total - compared with $40,000 for the later investor - the early investor ends up with more.

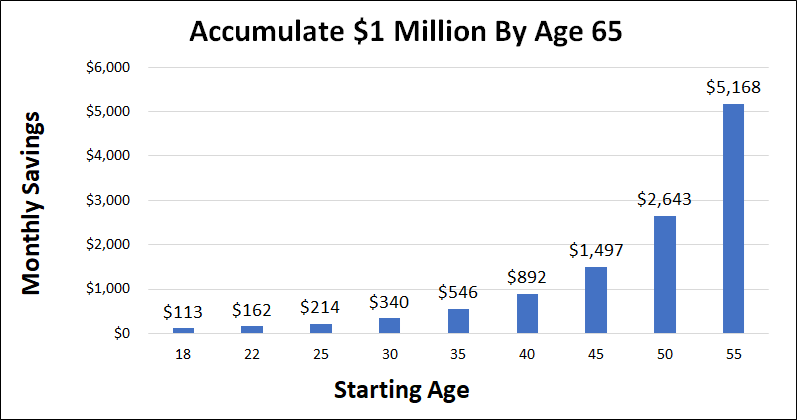

The bar chart below shows the monthly amount required to reach $1 million by age 65, assuming a 9% return.

(To save $2 million, simply double the amounts shown.)

Starting earlier means you need to save less each month. That part is intuitive - but it doesn’t fully explain why the difference is so dramatic.

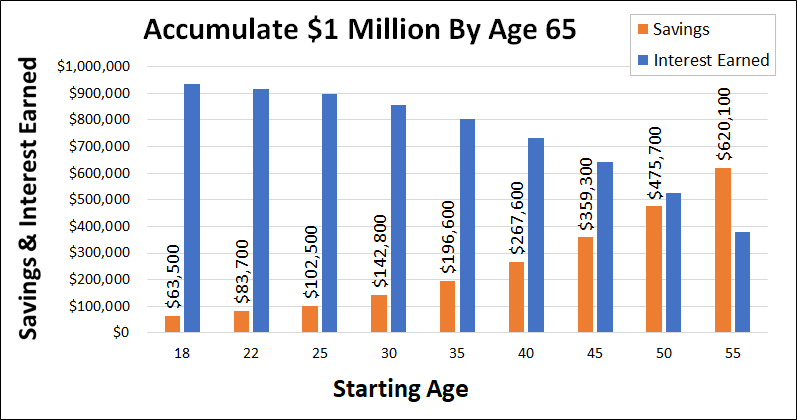

The chart below breaks the $1 million into two parts: what you contribute from your own income (labeled “savings”) and what comes from investment growth (labeled “interest earned”).

Starting at age 18, you would invest for 47 years and contribute about $63,500 in total (47 years x 12 months x ~$113). The remaining $936,500 - nearly all of the $1 million - comes from compound growth.

Starting later flips that balance, requiring far more of the total to come from your own contributions.

Starting earlier doesn’t just reduce how much you need to save each month - it dramatically reduces how much of your own money you need to contribute over a lifetime. Time does the heavy lifting.

That’s the advantage of compounding, and it fades with age.